Dispersion Strategies Demystified: Quant Evidence and Applications

Dispersion trading is a strategy that leverages the difference between index option volatility and individual stock option volatility. Here's how it works:

- Core Idea: Sell index options (lower implied volatility) and buy individual stock options (higher implied volatility).

- Why It Works: Index volatility is often lower because individual stock movements cancel each other out.

- When It Works Best: Calm markets with active stock-specific events, like earnings announcements.

This approach allows traders to profit from volatility differences without depending on market direction. However, it requires careful risk management, such as delta hedging and monitoring correlation spikes, to address challenges like gamma risk and execution costs. Advanced tools, like TraderVPS, can help traders optimize execution and manage risks efficiently.

Key insights:

- Focus on implied vs. realized volatility gaps.

- Backtests show strong returns, but execution costs can impact profitability.

- Infrastructure, like low-latency VPS, is crucial for managing complex trades.

Dispersion trading offers a structured way to capture volatility opportunities, but success depends on precise execution and robust systems.

How Dispersion Strategies Work

Short Index Options vs. Long Single-Stock Options

Dispersion trades involve selling options on an index while buying options on individual stocks within that same index. For example, traders might sell index volatility - often using strategies like straddles or strangles on indices such as the S&P 100 - and simultaneously buy options on a selection of the index's components. The goal is to exploit the difference between the implied volatility of the index and the average implied volatility of its underlying stocks [5][6].

A typical dispersion trade involves short index volatility and long single-stock options, structured to be vega-neutral.

To manage risk, traders carefully design their stock baskets. Most aim for a vega-neutral position, which balances volatility exposure between the short index options and the long single-stock options. This ensures that profits or losses are driven mainly by changes in correlation rather than by directional market moves. Traders often use at-the-money (ATM) options or a range of strikes to focus on variance exposure while avoiding reliance on specific price paths [4].

Hedging plays a critical role in keeping these positions market neutral.

Delta Hedging and Neutrality

To maintain a market-neutral stance, traders rely on active delta hedging, which minimizes exposure to directional equity risk [7]. The long single-stock options leg is typically delta-hedged at the end of each trading day to neutralize directional risk [1][6]. However, even with vega-neutral positioning, market stress can still pose challenges. Correlation shocks during volatile periods often affect gamma exposure more than vega [5]. As a result, traders need to adjust their hedges dynamically throughout the day, which can drive up costs. For instance, the execution drag from frequent rebalancing can cost as much as 1.5 basis points per stock in a basket of 200 names, amounting to 300 basis points for a round-trip [5]. These adjustments are essential to achieve the primary objective of dispersion trades: capturing volatility differences between the index and its components.

Even with delta hedging, gamma risk requires careful attention.

Managing Vega and Gamma Risks

Traders size their positions based on vega exposure, ensuring that the portfolio reacts predictably to changes in volatility. However, gamma risk - especially during market stress - can still lead to losses despite vega neutrality [5]. To address this, traders often use gamma-flat or vega-flat strategies, which involve systematic adjustments to the basket's construction [4].

- A gamma-flat approach focuses on reducing exposure to individual stock variance while limiting correlation risk.

- A vega-flat strategy prioritizes managing overall volatility risk and the correlation premium.

Both approaches require tailored rebalancing schedules and continuous monitoring. By fine-tuning their hedging strategies, traders can minimize costs and maintain effective risk control, keeping the dispersion trade on track.

Data-Driven Evidence of Profitability

Implied vs. Realized Volatility Gaps

Dispersion strategies thrive by capitalizing on the difference between expected (implied) and actual (realized) volatility. Index options often carry a higher implied volatility compared to individual stock options, reflecting the embedded correlation risk premium. This creates a pricing gap that traders can exploit [1][3].

Evidence from the S&P 500 highlights this phenomenon: index options consistently show higher implied volatility than individual stock options. During periods of market stress, this gap tends to widen, making dispersion trades even more profitable.

These measurable advantages pave the way for a closer look at backtesting results.

Backtested Returns and Risk Premia

Backtesting results demonstrate that dispersion strategies can achieve strong, risk-adjusted returns - even when accounting for transaction costs. One study focusing on U.S. options (spanning October 31, 2005, to November 1, 2007) repeatedly captured both correlation and volatility risk premia, even under challenging market conditions [1][8].

Market inefficiencies and behavioral biases create additional opportunities for mispricing, which dispersion strategies are designed to exploit [1]. Another advantage is that these trades typically show a low correlation with broader market returns, offering diversification benefits. However, to sustain returns, careful attention must be given to managing issues like execution friction, funding costs, and liquidity differences [5].

Dispersion Trading as a Derivatives Strategy and How Realized Correlations Impact the Approach

How to Apply Dispersion Strategies

Theoretical vs Practical Dispersion Trading: Key Execution Factors

Execution Techniques

To put dispersion strategies into action, traders commonly sell short index variance swaps while purchasing single-stock variance swaps to take advantage of volatility differences [2][4].

Another popular approach involves using at-the-money (ATM) straddles. For example, a trader might sell an ATM straddle on the index while buying proportionate ATM straddles on individual stocks. This setup benefits when the stocks experience significant movement but the index stays relatively stable [10].

To maintain market neutrality and avoid directional risk, traders often rely on end-of-day delta hedging [7]. For those expecting more pronounced directional dispersion, out-of-the-money (OTM) options can sometimes better capture the "correlation smile" compared to ATM options. It’s also critical to focus on liquid stocks with tight spreads and align trades with broader market flows [5].

These strategies form the groundwork for refining performance through selective filtering.

Performance Enhancements

One effective way to refine performance is by leveraging analyst disagreement as a filter. Research from 1996 to 2007 demonstrated that sorting S&P 100 stocks into quintiles based on analyst disagreements about earnings - and then buying puts on stocks with the highest disagreement while selling index puts - can lead to improved returns [1]. High levels of disagreement often align with differences in implied volatility, creating opportunities for traders to exploit pricing inefficiencies.

A mid-2025 strategy provided further evidence of this approach’s effectiveness. By incorporating analyst disagreement, traders reduced exposure to overpriced volatility and concentrated on undervalued risk areas [7]. This blend of quantitative modeling and fundamental insights allows for a more targeted approach, avoiding inflated volatility while zeroing in on better opportunities.

Next, we’ll examine how idealized models compare to the realities of execution, shedding light on the practical challenges that impact strategy outcomes.

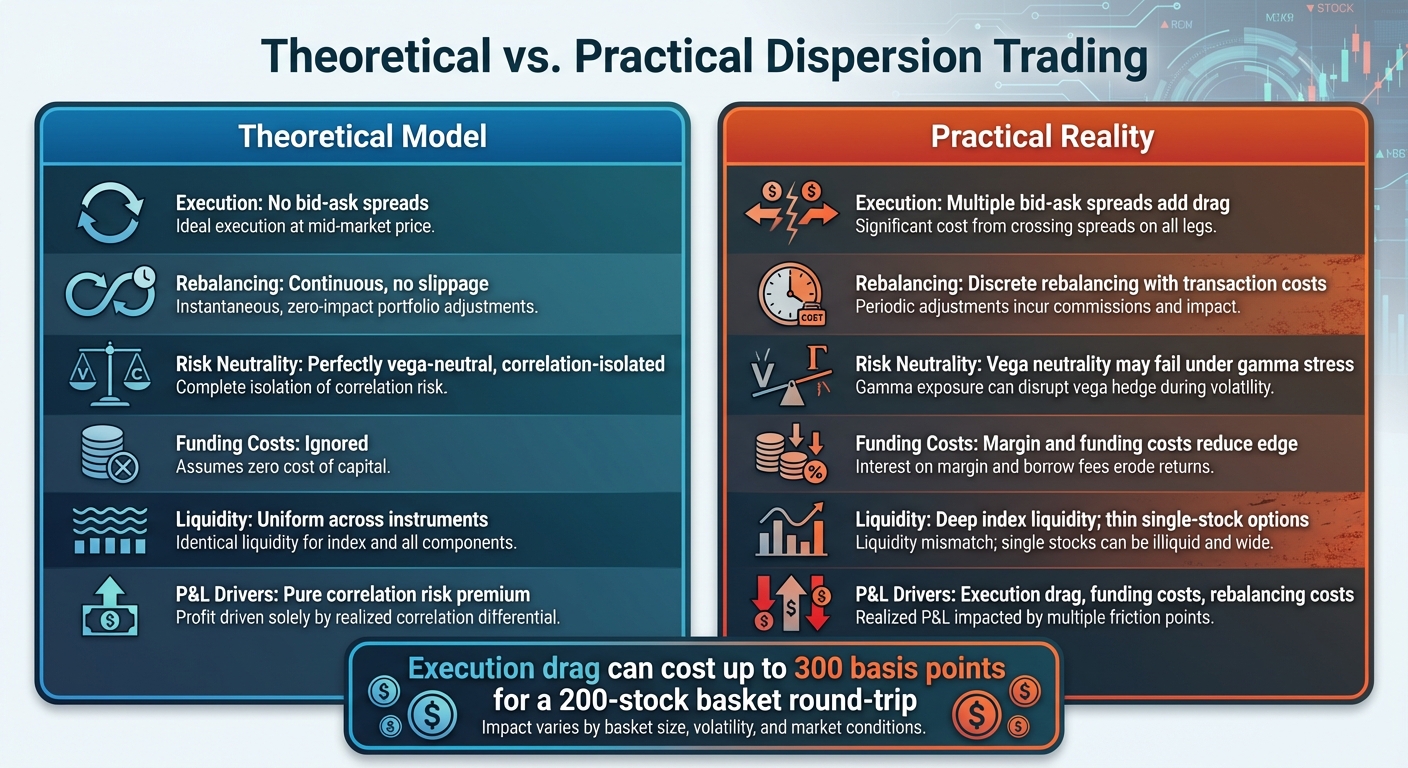

Comparing Clean vs. Practical Results

Practical challenges often complicate the clean execution assumed in theoretical models. While theoretical frameworks envision frictionless trading and continuous rebalancing, real-world constraints can significantly impact profitability. The table below highlights some of these discrepancies:

| Factor | Theoretical | Practical |

|---|---|---|

| Execution | No bid-ask spreads | Multiple bid-ask spreads add drag |

| Rebalancing | Continuous, no slippage | Discrete rebalancing with transaction costs |

| Risk Neutrality | Perfectly vega-neutral, correlation-isolated | Vega neutrality may fail under gamma stress |

| Funding Costs | Ignored | Margin and funding costs reduce edge |

| Liquidity | Uniform across instruments | Deep index liquidity; thin single-stock options |

| P&L Drivers | Pure correlation risk premium | Execution drag, funding costs, rebalancing costs |

Theoretically, a drop in correlation offers a clear variance advantage. However, in practice, these gains can be wiped out by execution drag, funding costs, and rebalancing inefficiencies unless the strategy is carefully tuned [5]. To mitigate these challenges, traders can use automated rebalancing to minimize transaction churn, size positions based on vega notional, and closely monitor gamma exposure during periods of stress [5].

As Quant Insider succinctly put it, "The 'dirty' in dirty dispersion is the alpha." The true edge lies in exploiting situations where flow imbalances cause index volatility to be systematically bid while single-stock volatility lags behind. Success depends on having infrastructure capable of managing and recycling risk faster than it decays [5].

Risk Management in Dispersion Trading

Managing Correlation Spikes

Dispersion trading carries a unique risk: sudden spikes in correlation among individual stocks. These spikes often occur during macroeconomic shocks, such as Federal Reserve announcements, geopolitical events, or periods of market panic. When correlations rise sharply, stocks tend to move in sync, which can disrupt strategies that depend on their independent behavior [6]. As Resonanz Capital explains:

If a macro shock drives correlations higher than implied, it loses [6].

Looking back at events like the 2008 financial crisis or the market turbulence during COVID-19, it’s clear how quickly assumptions about volatility can unravel. Keeping an eye on implied correlation indices, such as the CBOE COR1M or COR3M, becomes essential for identifying potential risks before they escalate.

To manage these correlation spikes, traders often hedge their positions by going long on correlation during chaotic periods and short during calmer times. Dynamic rebalancing helps maintain a balanced risk profile, while diversifying across liquid single-stock options provides an additional layer of protection [5]. This approach also requires careful position sizing and system readiness, both of which are crucial for navigating sudden market shifts.

Time Decay Benefits and Position Sizing

One advantage of dispersion trading is the time decay on sold index options, which can work in the trader’s favor. However, managing risks is equally important. Traders typically limit their exposure per trade to around 1%–2% of their capital and implement strict controls, such as leverage caps, stop-losses, and maintaining a minimum risk-reward ratio of 2:1 [9][11]. During periods of heightened volatility - think earnings announcements or major economic updates - reducing position sizes further helps to cushion against unexpected market swings. These risk controls are only effective when paired with a solid trading infrastructure, which we’ll explore next.

Infrastructure Requirements

Dispersion trading relies heavily on robust, low-latency systems to monitor risks and execute trades in real time [2]. Execution delays can be costly - when trading a basket of 200 stocks, for instance, round-trip execution drag can reach up to 300 basis points, significantly impacting potential returns [5]. Automated rebalancing systems help reduce unnecessary transaction churn, while real-time gamma monitoring ensures that positions stay within predefined risk limits. This is particularly important for managing both gamma and correlation risks during volatile market conditions.

The key to success lies in managing risks faster than funding and execution costs can eat into profits. For traders handling complex, multi-leg strategies, a reliable VPS solution is essential to maintain consistent connectivity and enable timely rebalancing, especially during periods of market turbulence.

Running Dispersion Strategies on NinjaTrader with TraderVPS

VPS Requirements for Dispersion Trading

Dispersion trading strategies demand a powerful VPS setup, especially for tasks like intensive backtesting and real-time delta hedging. NinjaTrader 8.1, for instance, leans heavily on strong single-core performance for execution. At the same time, multi-threading plays a key role in handling data loading, chart rendering, and backtesting [12]. To keep up, your VPS needs both high single-core speeds and enough RAM to manage the memory-heavy task of tracking multiple positions.

For moderate workloads - think 3–5 charts and basic backtesting - you’ll need at least 6 CPU cores and 16GB of RAM. If you’re working with more complex setups, like monitoring a large number of stocks or making dynamic adjustments, you’ll want 24+ cores and 64GB of RAM to avoid performance hiccups. Storage is another critical factor: NVMe SSDs ensure fast data access, which is crucial for retrieving historical volatility data or executing multi-leg orders without delays.

TraderVPS offers VPS plans specifically tailored to these performance demands.

TraderVPS Plans for Professional Traders

TraderVPS has designed its plans to meet the high computational and memory needs of dispersion trading on NinjaTrader. Here’s a breakdown of some of their plans:

- VPS Lite Plan ($69/month): Includes 4 AMD EPYC cores, 8GB of RAM, and 70GB of NVMe storage. This plan is perfect for simpler setups, such as running 1–2 charts.

- VPS Pro Plan ($99/month): Offers 6 cores, 16GB of RAM, 150GB of NVMe storage, and support for up to 2 monitors. This makes it a solid choice for traders tracking index options alongside single-stock positions.

- VPS Ultra Plan ($199/month): Provides 24 cores, 64GB of RAM, 500GB of NVMe storage, and support for up to 4 monitors. Ideal for managing larger portfolios or conducting intensive backtesting.

- Dedicated Server Plan ($299/month): Delivers top-tier performance with 12+ AMD Ryzen cores, 128GB of RAM, and 2TB+ of storage. This plan is designed for heavy-duty tasks like running multiple charts or managing several accounts simultaneously.

All plans come with 99.999% uptime and unmetered bandwidth, ensuring your trading strategies operate without interruptions.

TraderVPS’s Chicago datacenter offers ultra-low latency of less than 0.52ms to the CME Group exchange, which is a game-changer for futures trading. As TraderVPS explains:

Our Chicago datacenter delivers lightning-fast latency (<0.52ms) directly to the CME exchange, facilitating quicker futures trade execution and substantially reducing slippage [13].

Optimizing Strategy Execution with TraderVPS

TraderVPS doesn’t just provide powerful specs - it also includes features that directly enhance your trading performance. For example, NVMe storage speeds up data processing, which is critical for strategies that rely on real-time analysis. Additionally, their robust DDoS protection and advanced firewall settings protect your operations from external threats, ensuring uninterrupted execution for automated strategies.

The platform supports multi-monitor setups, allowing you to track index volatility, individual stock positions, and correlation metrics across multiple screens. This setup helps you spot correlation spikes before they affect your portfolio. Plus, their 24/7 technical support team, based in the U.S., is always available to resolve any issues quickly - an essential service during volatile market conditions.

TraderVPS is also compatible with all major futures market data feeds, including Rithmic, CQG, and IQFeed. This ensures fast and reliable data transmission, which is crucial for real-time gamma monitoring and other advanced trading needs.

Conclusion

Key Insights on Dispersion Trading

Dispersion trading takes advantage of the pricing gap between the higher implied volatility of index options and the typically lower volatility of individual stocks. The real opportunity lies in capitalizing on the persistent gap between implied and actual correlations over time [6].

That said, it’s not without its challenges. Managing execution friction across hundreds of single-stock options, addressing complex gamma risk during volatile periods, and dealing with liquidity differences between deep index options and less liquid single-stock positions are all critical hurdles [5]. In practice, the true edge comes from leveraging flow imbalances while maintaining an infrastructure capable of managing risk efficiently and keeping costs under control [5]. These factors highlight why having a robust execution infrastructure is absolutely essential.

Final Thoughts on Implementation

Given these challenges, a strong execution infrastructure is indispensable. Real-world factors like execution drag, funding costs, and gamma risk can quickly eat into theoretical gains [5]. Dispersion trading, as discussed, demands cutting-edge execution technology, and TraderVPS offers a solution tailored to meet these needs.

With plans starting at $69/month for simpler setups and scaling up to $299/month for more demanding multi-account operations, TraderVPS provides the computational power and ultra-low latency required for automated rebalancing, real-time risk management, and precise order execution. Its infrastructure - featuring high-performance components, NVMe storage, and 24/7 uptime - ensures your strategy runs smoothly without interruptions. For professional futures traders using platforms like NinjaTrader to execute dispersion strategies, this level of performance can be the difference between theoretical potential and consistent profitability.

FAQs

What are the main risks associated with dispersion trading?

Dispersion trading comes with its own set of risks, and traders need to approach it with caution. One of the biggest challenges is dealing with extreme market volatility, especially during financial crises. When markets spiral, poorly managed positions can lead to heavy losses. Another issue is the surge in correlation spikes during downturns, which can weaken the expected diversification benefits that these strategies typically rely on.

On top of that, there’s the danger of mispricing assets or the sudden unwinding of positions, both of which can cause significant financial setbacks. To navigate these hurdles, having strong risk management strategies in place is absolutely essential for safeguarding portfolios.

What role does delta hedging play in keeping dispersion strategies market-neutral?

Delta hedging is a technique designed to neutralize market risk by offsetting the directional exposure of options. By continuously adjusting the hedge position in response to changes in the underlying asset's price, it helps keep the portfolio's sensitivity to overall market movements as low as possible.

This method is particularly useful in dispersion strategies, where the goal is to capitalize on volatility and correlation differences rather than being influenced by larger market trends. The outcome is a more focused and controlled trading approach that targets specific opportunities while keeping risk in check.

Why is having a low-latency infrastructure important for successful dispersion trading?

Low-latency infrastructure plays a key role in dispersion trading by ensuring trades are executed swiftly and efficiently. This reduces delays, cuts down on slippage, and allows traders to react instantly to sudden market shifts.

With faster execution, traders can capitalize on brief arbitrage opportunities and make quick adjustments to their positions during volatile market conditions. This approach not only boosts potential profits but also improves risk management - an essential aspect of successful dispersion trading.